Read two articles tonight that seemed apparently contradictory. One was an

article in the WSJ today about how the Fed is shifting its focus from the benign inflation readings of the past few weeks (somewhere in the 1 - 2% range) to future inflation because of low unemployment. Makes sense right? Low unemployment means higher demand which means higher prices which means inflation. I immediately read an

editorial by Steve Forbes in Forbes magazine called "Do Bad Economic Ideas Ever Die?" where he talked about how for some reason people still think that the ecomonic trade-off between inflation and unemployment holds. Here's an excerpt from the Forbes article:

The current concern about inflation sadly confirms the staying power of bad ideas, in this case the notion that economic growth creates inflation. The Phillips curve, which posits that there is a tradeoff between inflation and unemployment, has long been discredited by events and academic research. Since Ronald Reagan became President in 1981, for example, the U.S. has had a fantastic expansion, and inflation virtually disappeared until recently. Yet the media are full of stories and pundit head shaking that global capacity for producing goods could soon run out.

Indeed, the

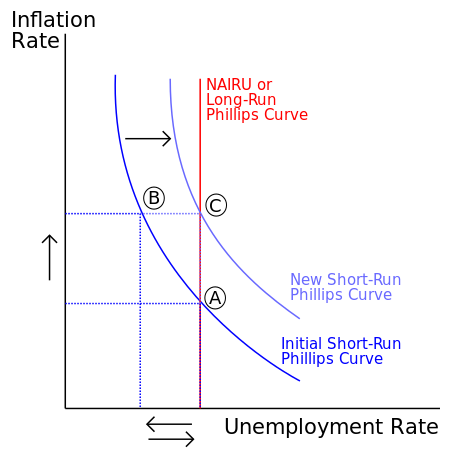

Phillips Curve was on my final test for my

Essentials of Economics class. In the short-run, there is definitely a trade-off between inflation and unemployment, but that trade-off just doesn't exist in the long-run. Here's an excerpt from Wikipedia:

Most economists no longer use the Phillips curve in its original form because it was shown that it simply did not work. This can be seen in a cursory analysis of US inflation and unemployment data 1953-92. There is no single curve that will fit the data, but there are three rough aggregations—1955-71, 1974-84, and 1985-92—each of which shows a general, downwards slope, but at three very different levels with the shifts occurring abruptly. The data for 1953-54 and 1972-73 does not group easily and a more formal analysis posits up to five groups/curves over the period.

These days, however, a modified Phillips Curve is very prevalent. This new form incorporates inflationary expectations, pioneered by Edmund Phelps and Milton Friedman. This new view of the Phillips curve agrees that in the long run policy cannot affect unemployment, for it will always readjust back to its "natural rate." However, this new Phillips Curve does allow for short run fluctuations and the ability of a monetary authority such as the central bank to temporarily decrease unemployment for an increase in inflation, and vice versa.

So why am I pointing this out? Mostly just because I can't believe I actually knew what they were talking about. Education. Gotta love it.

Read two articles tonight that seemed apparently contradictory. One was an article in the WSJ today about how the Fed is shifting its focus from the benign inflation readings of the past few weeks (somewhere in the 1 - 2% range) to future inflation because of low unemployment. Makes sense right? Low unemployment means higher demand which means higher prices which means inflation. I immediately read an editorial by Steve Forbes in Forbes magazine called "Do Bad Economic Ideas Ever Die?" where he talked about how for some reason people still think that the ecomonic trade-off between inflation and unemployment holds. Here's an excerpt from the Forbes article:

Read two articles tonight that seemed apparently contradictory. One was an article in the WSJ today about how the Fed is shifting its focus from the benign inflation readings of the past few weeks (somewhere in the 1 - 2% range) to future inflation because of low unemployment. Makes sense right? Low unemployment means higher demand which means higher prices which means inflation. I immediately read an editorial by Steve Forbes in Forbes magazine called "Do Bad Economic Ideas Ever Die?" where he talked about how for some reason people still think that the ecomonic trade-off between inflation and unemployment holds. Here's an excerpt from the Forbes article:

Comments